The conventional wisdom today is that Facebook is a mature behemoth that is under intensifying risk of being penalised in a multitude of possible ways by regulators.

It is certainly a behemoth. The scale of Facebook really is quite difficult to imagine. Every month, more than three billion of us interact with at least one of its properties – from the traditional Facebook Blue newsfeed, to Instagram, to WhatsApp to Facebook Messenger. Each day, users spend more than 100,000 collective years on Facebook properties.

Network effects lead to domination

Facebook’s primary business model to date has been one of digital advertising – which drives substantially all of the company’s US$75 billion in annual revenues. And this has been a powerful business model driven by substantial network effects: the more users that engage with Facebook’s properties, the more valuable the platform becomes to each existing user, driving more user growth. The more user growth, the more data Facebook collects, the more effective targeting Facebook can provide digital advertisers, the higher advertiser ROIs, the more ad spend Facebook attracts and the higher its revenues.

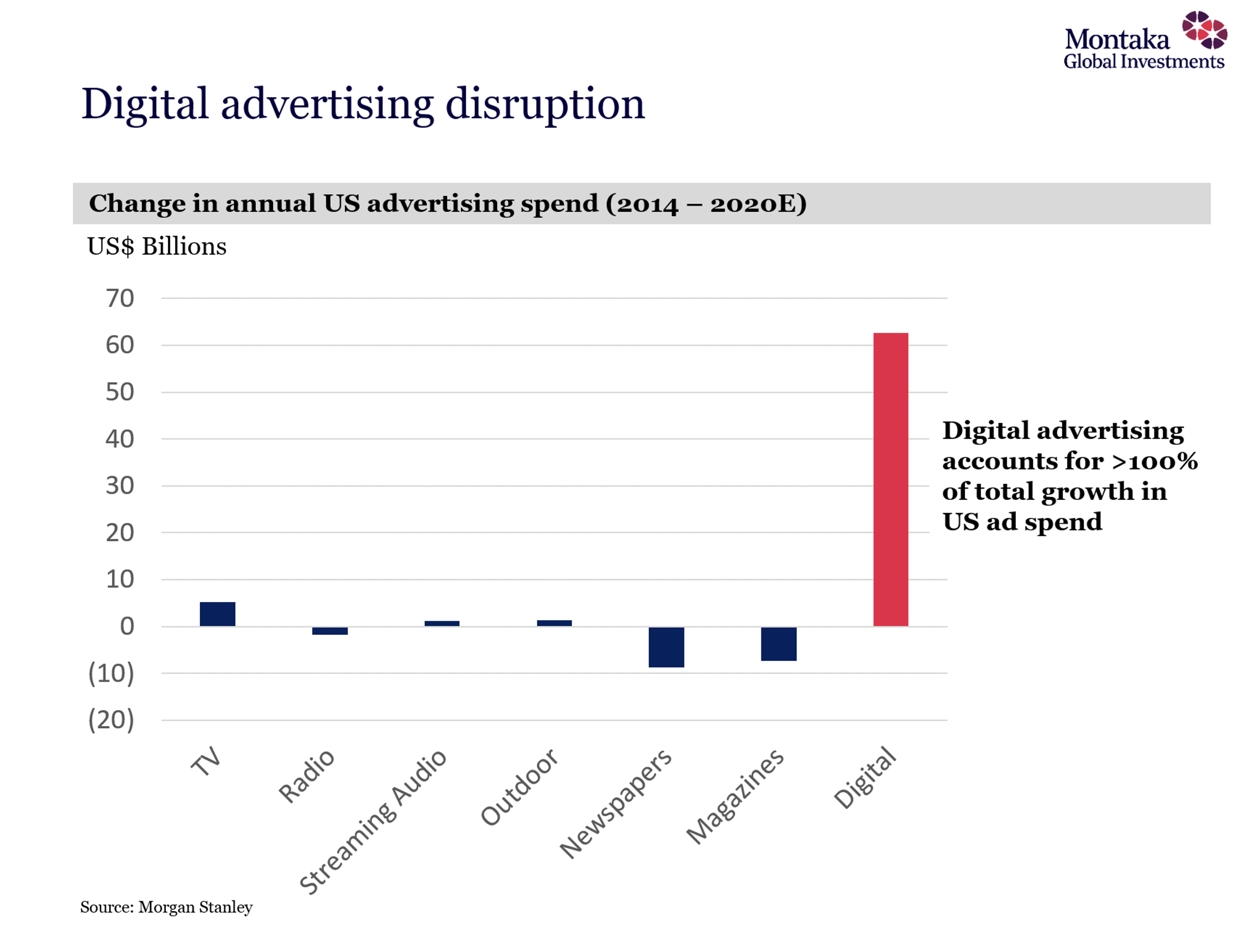

It is this dynamic that has resulted in digital advertising spend dominating all other forms of advertising over recent years, as illustrated below. And this trend is set to only continue. In interviews conducted by Montaka’s investment team, we continually hear from allocators of digital advertising budgets that Facebook consistently scores the highest ROIs, compared to competing digital platforms. It is perhaps not surprising, therefore, that Facebook’s revenues have increased by approximately 15x since 2012!

Resilience in the face of a pandemic

A powerful learning from the ongoing COVID-19 crisis is the extraordinary resilience of Facebook’s advertising business model. In the depths of a global pandemic and with US GDP growth down 10 percent, Facebook’s advertising revenue still grew in the double-digits percent versus the same time in the prior year. And let’s not forget that advertising is typically viewed as a discretionary expense by many businesses: it is often the first expense to be cut when times are tough.

But for many businesses – particularly small and medium sized businesses (SMBs) – cutting spend on Facebook often translates directly into reduced sales. This is key. With Facebook’s superior measurability, digital marketers can much more accurately assess whether or not ad spend is translating into sales. If not, spend is cut; if so, spend is increased. This optimisation process has turned Facebook into the ultimate customer acquisition machine for many SMBs. Without Facebook, these businesses simply cannot acquire their customers – and would, therefore, miss out on sales.

An evolving business model?

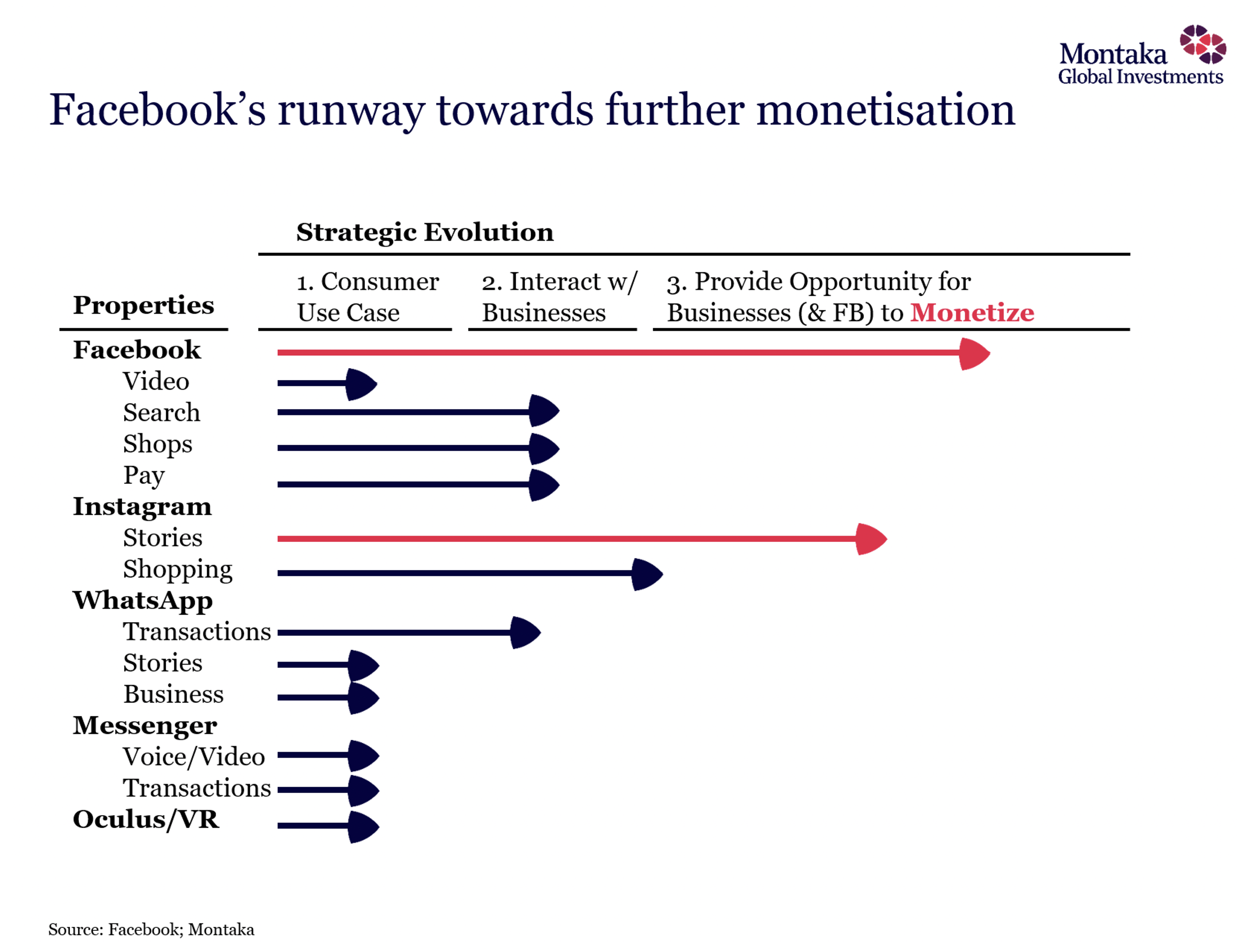

If Facebook effectively owns the SMB customer, why stop at advertising? Why not facilitate complete transactions on Facebook’s properties? And this is exactly what Mark Zuckerberg and Sheryl Sandberg have in mind.

At the end of last month, Zuckerberg introduced Facebook Shops to investors. Shops allows any SMB to create an immersive full screen storefront with a catalogue on the Facebook platform. Initially, this will translate into a shop front on Facebook and Instagram, but over time, the shop front will appear on all Facebook properties. Facebook members – all 3.1 billion of them – can discover products in shops, interact with SMBs via Messenger and WhatsApp and then transact using Facebook Pay.

Apart from the obvious incremental revenue opportunity from sharing in e-commerce transactions, there is a very important, albeit less obvious, benefit to this new business model: closing the loop. SMBs will be able to track the efficacy of ad spend even more directly by tracing it all the way through to point of sale. These insights are valuable for marketers. And, of course, higher-value advertising comes at higher prices without eroding the ROI to the marketer. In a sense, everybody wins.

Facebook remains in its early days of monetisation

It is truly extraordinary that a US$700 billion business could still be in its early days of growth. And yet, this is an argument that is worth consideration. It is a fact that most of Facebook’s properties are yet to be monetised, as we detail below. Even within Facebook’s traditional advertising business, its monetisation penetration of SMBs remains surprisingly low: of the 180 million businesses that use Facebook’s properties every month, only nine million advertise with Facebook today. That number will only increase.

For all the talk of the sun setting on Facebook, we believe it is more likely that the sun is rising. We believe in owning the long-term winners in attractive markets. And with Facebook’s extraordinary reach and continually growing data advantages, the probability of Facebook winning for decades to come is very high.

Would you invest in Facebook? In the depths of a global pandemic, Facebook’s advertising revenue still grew in the double-digits versus the same time in the prior year. Andrew shares his investment thesis. Click To Tweet

The Montgomery Global Funds and Montaka own shares in Facebook. This article was prepared 26 August with the information we have today, and our view may change. It does not constitute formal advice or professional investment advice. If you wish to trade Facebook you should seek financial advice.

We are delighted to announce the launch of the Montaka Global Extension Fund (Quoted Managed Hedge Fund) (ASX: MKAX). This new fund gives investors access to a portfolio of global growth opportunities through one online trade. You can also register to receive more information about the fund here: MKAX: Register Your Interest